Since its inception, Tesla (NASDAQ:TSLA) has been defying norms and pushing boundaries. Its ambitious mission to “accelerate the world’s transition to sustainable energy” has propelled it to the forefront of the global EV industry. However, the TSLA stock narrative extends beyond its prowess in EV manufacturing. Its foray into areas such as autonomous driving technology, energy storage, and solar power positions it as a diversified technology player that rivals traditional tech giants in terms of potential growth and market influence.

This blend of car manufacturing and technology innovation has led some analysts to label Tesla not merely as a carmaker, but as a technology conglomerate in the making.

Here’s the problem – for all the company’s strengths, investors seemingly are unable to understand there is a difference between a company and a stock, let alone a man and a company, and margin compression is going to be a bigger and bigger deal over time.

A Roller-Coaster Year for TSLA Stock

While Tesla’s operational performance has been impressive, its stock performance in 2023 has been nothing short of a roller-coaster ride. After a period of price cuts that caused automotive margins to plummet and share prices to take a hit, Tesla’s stock has made a remarkable recovery, soaring by over 160% in 2023.

This rally, however, raises concerns about overvaluation. Tesla’s stock price appears to be moving not based on fundamentals, but rather on the inability of investors to distinguish between the stock, the company, and Elon Musk. This conflation of factors could be inflating Tesla’s valuation, rendering it overpriced and potentially risky for investors.

Trouble in Paradise: Tesla’s Margin Dilemma

In recent months, Tesla has been grappling with margin pressures due to aggressive price cuts aimed at boosting vehicle demand. These price reductions have led to a steep decline in Tesla’s automotive gross margins, from 32.9% in Q1 2022 to 21.1% in Q1 2023.

Tesla’s management has adopted a strategy of prioritizing volume growth over margins with the belief that the company can eventually drive profitability through its autonomous driving software. While this approach may yield long-term benefits, it poses significant short-term risks, particularly if Tesla fails to deliver on its full self-driving (FSD) promises.

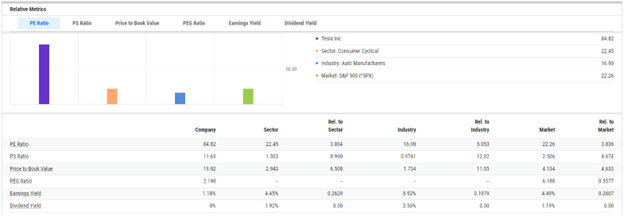

This, combined with fundamentals which are significantly overvalued, should give true longer-term investors pause. A look at relative valuations metrics from YCharts suggests Tesla is overvalued by many metrics.

Ultimately, the Tesla enigma — the complex interplay between the company, its stock, and its charismatic CEO — presents both challenges and opportunities for investors.

The task at hand is to unravel this enigma, understand the underlying dynamics, and make informed investment decisions based on a holistic understanding of Tesla’s business, growth prospects, and potential risks. I’m personally not a big fan of investments that are untethered from fundamental reality.

Margin pressure and the inability for investors to understand that Elon Musk is not Tesla alone makes me worry that Tesla won’t need much to begin an aggressive correction, which in turn could have larger implications on the broader stock market.

On the date of publication, Michael Gayed did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.